Dubai’s largest port operator, DP World, has appointed a new CEO after revelations surfaced about the former chief’s past association with the late financier Jeffrey Epstein.

The company announced on Friday that Essa Kazim would serve as chairman of the board, while Yuvraj Narayan takes over as group Chief Executive Officer, replacing Sultan Ahmed bin Sulayem.

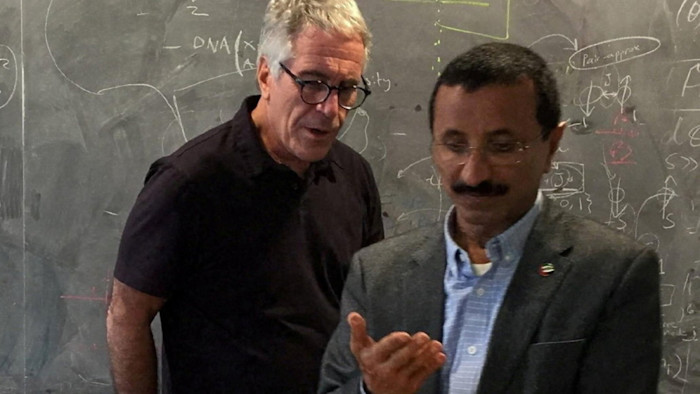

The disclosure follows the U.S. Department of Justice’s recent release of documents showing that Epstein once described Sulayem as a “close personal friend” and one of his most trusted associates. Sulayem has not faced any criminal charges related to Epstein.

A filing to Nasdaq Dubai, where DP World maintains listed bonds, confirmed Sulayem’s resignation “effective immediately.” He had served as chairman since 2007 and CEO since 2016.

The company said the new appointments aim to support sustainable growth, strengthen global supply chains, and reinforce Dubai’s position as a leading trade and logistics hub, without directly mentioning Sulayem.

Kazim previously served as Governor of the Dubai International Financial Centre, while Narayan had been DP World’s deputy CEO and CFO since 2005. Sulayem, a prominent figure from one of Dubai’s influential families, was instrumental in transforming Jebel Ali port into a major global shipping hub and expanding DP World into an international logistics empire handling roughly a tenth of the world’s container trade.

He also previously led Nakheel Properties but was replaced following a major board restructuring during Dubai World’s debt crisis in 2008.

The Epstein files revealed that Sulayem maintained contact with the convicted financier even after Epstein’s 2008 conviction for soliciting prostitution from a minor. Their communications reportedly included business discussions, requests for advice on meetings and investments, and references to sexual encounters and escort services. Authorities have emphasized that inclusion in the files does not imply wrongdoing or involvement in any criminal activity.

Pressure on Sulayem escalated after several international partners paused new deals with DP World. Canada’s La Caisse, which has invested over $5 billion alongside DP World in the past decade, stated it would halt additional capital deployment until the company addressed the situation.

Similarly, British International Investment, which co-invests with DP World in African ports, announced it would pause new investments pending the company’s response.

The company’s partners emphasized the importance of distinguishing between DP World as an entity and the former CEO personally, urging the board to take appropriate action.