Rising financial strain is weighing on Ghana’s cocoa industry, as licensed buying companies owe banks between $650 million and $750 million, industry representatives say. The heavy debt burden is tightening cash flow across the supply chain at a time when banks are still rebuilding after a deep economic crisis.

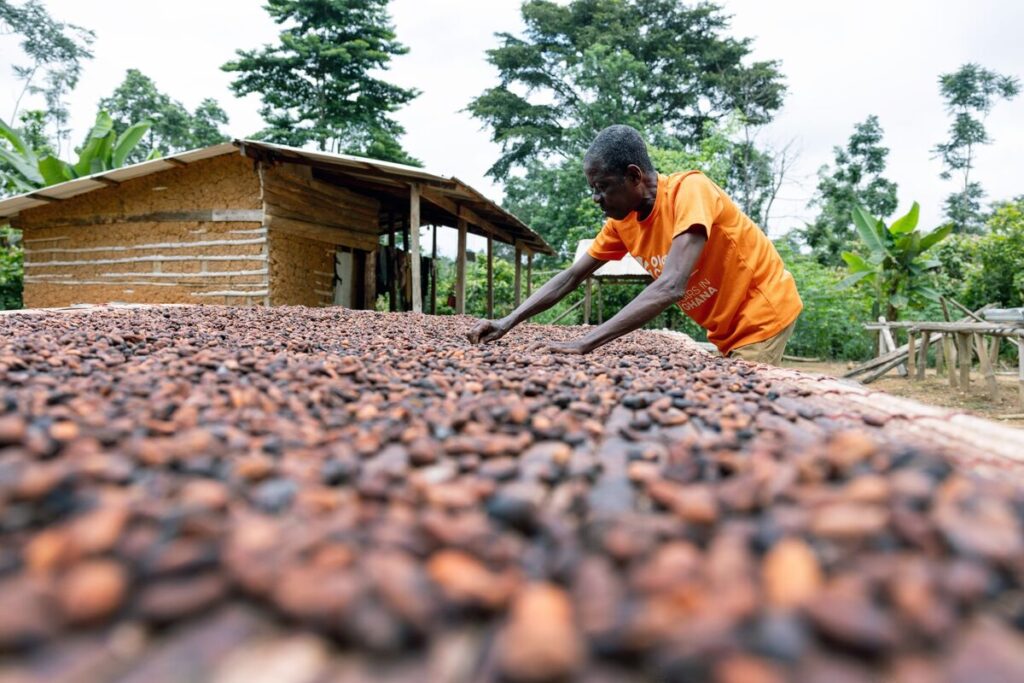

Ghana, the world’s second-largest cocoa producer after Ivory Coast, depends heavily on the crop for export revenue. Together, the two countries account for roughly half of global cocoa supply.

The sector has been hit by back-to-back weak harvests, driven by diseases such as swollen shoot virus and adverse weather conditions. At the same time, global cocoa prices have tumbled from peaks near $12,000 per tonne in 2024 to about $4,000 today, reflecting softer demand and expectations of improved future supply.

To pre-finance purchases from farmers, licensed buyers have borrowed heavily from banks, with total debts estimated at 7–8 billion cedis ($650–$750 million) to financial institutions and an additional $205–$234 million owed directly to farmers. “Interest keeps piling up,” said Samuel Adimado, president of the Licensed Cocoa Buyers Association.

So far this season, buyers have delivered around 580,000 metric tonnes of beans to the Ghana Cocoa Board (Cocobod), while another 70,000 tonnes remain unharvested. The recent cut in the farmgate price to $3,580 per tonne will affect roughly 100,000 tonnes, part of efforts to make Ghanaian cocoa more competitive after earlier high prices left stock unsold.

Government interventions include the mid-February 2026 price adjustment and plans for a new domestic cocoa financing scheme, potentially through cocoa bonds, aimed at easing cash flow pressures. Adimado noted that part of the debt buildup stems from Cocobod diverting funds to non-core activities such as road construction.

The banking sector is feeling the strain, with some loans restructured and potential losses looming. John Awuah, CEO of the Ghana Association of Banks, said the financial system remains resilient but requires careful oversight to align with Ghana’s IMF programme.

These challenges are rooted in broader issues, including the 2023 Domestic Debt Exchange Programme, which converted short-term instruments like Cocobod cocoa bills into longer-dated bonds at lower rates, reducing bank capital and contributing to sector stress.

The crisis underscores the need for stronger financial discipline at Cocobod and better alignment with global market realities to protect Ghana’s cocoa industry and the smallholder farmers who rely on it.